What Most Veterans Don’t Know About Their VA Home Loan Benefit

Nearly half of Veterans (49%) feel homeownership is currently out of reach, according to a recent survey from NewDay USA. But many are closer than they think. And you might be, too.

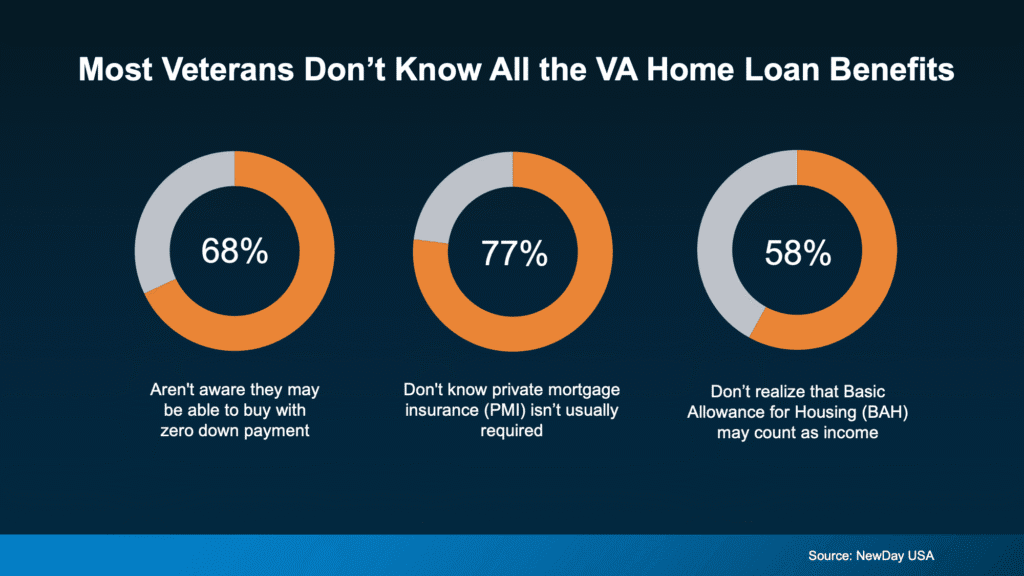

If you’re a Veteran, you probably know the VA home loan benefit exists. It’s been around for over 80 years. What you might not know is what it actually covers. Three misconceptions trip up Veterans the most:

Alt text: Chart showing VA loan misconceptions: 68% of Veterans don’t know they can buy with zero down payment, 77% don’t know PMI isn’t required, and 58% don’t realize BAH may count as income. Source: NewDay USA.

Any one of those beliefs could be holding you back. Let’s walk through all three so you have the information you really need.

You May Not Have To Put Any Money Down

The potential to put zero money down is probably the biggest perk of a VA loan, but most homebuyers don’t even realize that’s an option. According to the NewDay USA survey, 68% of Veterans aren’t aware they may be able to buy with zero down payment. Many respondents guessed they’d need to save somewhere between $10,000 and $19,900 before they could buy. That’s years of saving for an upfront cost that isn’t always required.

You May Have Lower Closing Costs

According to the Department of Veterans Affairs, VA loans can include limits on the types of closing costs buyers have to pay. That means more money stays in your pocket on closing day and less to save before you can buy. Combined with the zero down payment option, this can significantly speed up your buying timeline.

Your Monthly PMI Costs Could Be $0

Unlike many other loan options, VA loans typically don’t require private mortgage insurance (PMI), even with low or no money down. If you take out a conventional loan instead, you could pay $100 to $300 a month in PMI until you hit 20% equity, according to NewDay USA. Over time, that’s a difference of thousands of dollars. The NewDay USA survey found that 77% of Veterans don’t know PMI isn’t usually required on a VA loan. That’s a monthly cost that doesn’t have to exist.

Your BAH and BAS May Help You Qualify for More

If you’re on active duty or a qualifying reservist, your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward income qualification on a VA loan. That matters more than most people realize.

Here’s a simple example: if your BAH is $2,000 per month, that’s $24,000 per year in non-taxable income that a lender can factor into your qualifying calculation. Because it’s non-taxable, lenders are often able to gross it up, meaning it can carry even more weight than the same amount of taxable income would.

According to the NewDay USA survey, 58% of Veterans don’t know BAH can count as income. If you’ve been running the numbers without including it, you may qualify for significantly more than you thought, and your buying timeline could be closer than you expected.

If you’re stationed at or near Luke Air Force Base, or anywhere in the Phoenix metro, I work with Veterans and active duty buyers across the Valley and can walk you through exactly what your benefit covers and what you’d qualify for here in Arizona.

Bottom Line

VA home loans can put homeownership within reach, and the details matter. Zero down payment, no PMI, and military allowances that count toward your qualifying income are three advantages too many Veterans leave on the table simply because they didn’t know they existed.

If you’re active duty, you’ve served, or you know someone who has, connect with a lender who understands the VA benefit and can walk you through whether you’d qualify and what it means for your specific situation. You may be able to buy a home sooner than you thought.

Call to Action

Find out what your VA benefit actually means for your buying power.

A lot of Veterans are surprised by what’s possible once we actually sit down and run the numbers. No down payment, no PMI, and BAH that counts toward your qualifying income. That combination changes things quickly.

If you’re a Veteran, active duty, or a Realtor working with military buyers in the Phoenix area, let’s talk. I’ll show you exactly where you stand and what’s possible.

Schedule your Mortgage Strategy Call here: https://kevinbrierton.com/call

{kind=link}