Turning Your Realtor Relationship Into a Long-Term Real Estate Wealth Relationship

Most people think of a Realtor as the person who helps them buy or sell a home.

That is true, but I think that view is too small.

The right Realtor should be much more than a transaction guide. They should be a long-term real estate advisor. Not in the sense of replacing a CPA or financial advisor, but in the sense of helping you make better housing decisions over time. Decisions that match your lifestyle, your cash flow, your goals, and your future.

As a lender, I see this all the time. A client comes in focused on one thing: “Can I get approved?” That matters, of course. But the better question is this: “How do I make this housing decision work for me not only today, but over the next 5, 10, or 20 years?”

That is where a great Realtor becomes incredibly valuable.

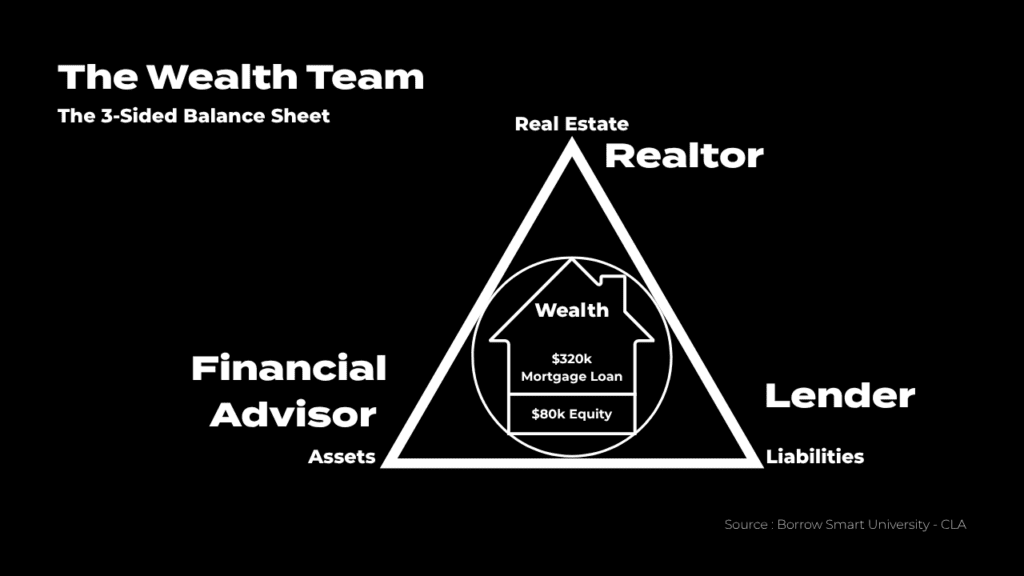

In the Borrow Smart framework, the strongest outcomes happen when the Realtor, lender, and advisor work together around what is called the 3-sided balance sheet. The idea is simple. Real estate decisions should not be made in isolation. They should connect to your liabilities, your available cash, your long-term goals, and your bigger financial life.

If you want to talk through your next move, purchase, refinance, or long-term housing strategy, schedule a mortgage strategy call here: CLICK HERE

That is a very different conversation than simply opening doors and writing offers.

A strong Realtor helps you think beyond the purchase.

They help you think about where you are in life. Are you likely to stay in the home for 3 years or 10? Are you planning for kids? Do you expect a job change? Will aging parents eventually need to live with you? Are you trying to preserve cash after closing? Do you want flexibility for a future move, renovation, or investment opportunity?

Those questions matter because your home is not only a place to live. It also impacts your cash flow, your liquidity, and the opportunities available to you later.

The CLA and Borrow Smart material breaks mortgage and liability planning into 7 steps: Product, Payment, Availability, Amount, Management, Protection, and Discipline. In plain English, that means the right home strategy is about more than rate. It is about choosing the right loan product for your time horizon, the right payment strategy for your goals, the right amount of cash to keep available, and the right support system after the closing is done.

That last part is where the best Realtors stand out.

A lot of people buy a home and then disappear into life. They do not revisit the decision until they want to move, rates drop, or a problem shows up. But the best Realtors stay in the relationship. They continue to be a resource. They check in as life changes. They help you see what options may be available before a decision becomes urgent.

That is real value.

If you want to talk through your next move, purchase, refinance, or long-term housing strategy, schedule a mortgage strategy call here: CLICK HERE

The Borrow Smart material also teaches that the mortgage conversation should include both today’s opportunities and tomorrow’s opportunities. The process is built around interview, conversation, and results. First, you gather facts and understand the client. Then you identify what matters now and what may matter later. Finally, you show the impact of a recommendation in a clear way.

That is exactly how a great Realtor should think.

For example, a young couple buying their first home may assume the goal is to put as much down as possible to keep the payment low. But what if that leaves them with too little liquidity after closing? What if keeping more cash available gives them flexibility for repairs, a future child, or another opportunity? One of the Borrow Smart case studies specifically shows how modeling different down payment strategies can help clients understand the tradeoff between payment savings and keeping cash in reserve.

That is not a small detail. That is a long-term wealth decision.

Another case study involved a couple nearing retirement who wanted to maximize savings before trading down in five years. The recommendation was not simply about financing a home. It was about structuring liabilities in a way that improved monthly cash flow and aligned with their retirement timeline.

Again, that is more than a transaction. That is planning.

This is why I believe clients should look for a Realtor who wants to stay in the relationship, not only win the deal.

The best Realtors are thinking ahead with you. They understand that real estate is part of your life plan. They know a home can create opportunity, but only if the decision is structured the right way and supported by the right team. They stay connected enough to help you think through the next move before you are forced into it.

And when that Realtor is working with the right lender, the value grows even more.

As a lender, my job is not simply to quote a rate and get a file closed. My job is to help clients understand how financing decisions affect cash flow, liquidity, and future flexibility. When a strong Realtor and a strong lender work together, clients get a much better experience. They are not only being told what they can do. They are being guided through what may make the most sense.

That is the difference between a sales relationship and a wealth relationship.

Your Realtor should not disappear after closing.

They should be someone you can come back to when life changes, when your goals shift, and when you need help making the next smart move in real estate.

That is the kind of partnership that creates confidence.

And over time, that kind of relationship can become one of the most valuable parts of your financial life.

If you want to talk through your next move, purchase, refinance, or long-term housing strategy, schedule a mortgage strategy call here: CLICK HERE

{kind=link}